De Minimis Benefits are tax exempt. These benefits were outlined and defined by the Bureau of Internal Revenue (BIR) in the issuance of Revenue Regulation No. 3-98 and several amendments since its adoption such as RR No 8-2000, RR No. 15-2011, RR No. 8-2012, RR No. 1-2015 and the latest issuance as of this writing is RR No. 3-2015.

De Minimis Benefits are tax exempt. These benefits were outlined and defined by the Bureau of Internal Revenue (BIR) in the issuance of Revenue Regulation No. 3-98 and several amendments since its adoption such as RR No 8-2000, RR No. 15-2011, RR No. 8-2012, RR No. 1-2015 and the latest issuance as of this writing is RR No. 3-2015.

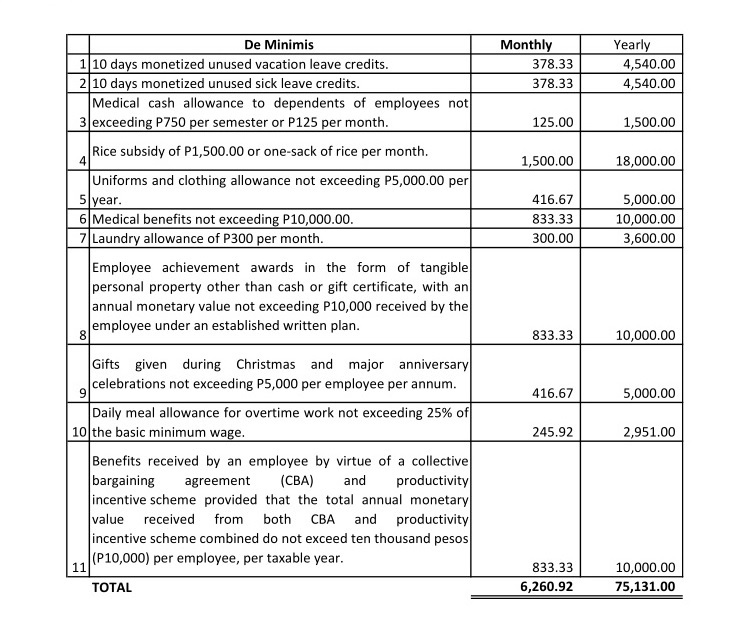

There are several sites discussing the topic and even the BIR per se. But how much really is the maximum amount of the benefits if we convert these into peso amount on a monthly or yearly basis?

The table below will give you a guide on the peso amount assuming a Minimum Wage Earner located in NCR or a daily wage of P454.00.

But then gain in the application of de minimis benefits, its important to note the stated limits. Further, it is also important to consider policies created by the company such as (1) Sick & Vacation Leave (SLVL) and (2) Health policy covered by an HMO. Lastly, it is important as well to finally consider if a company is under a CBA agreement.

Bottom line, De Minimis Benefits were created as employees privileges and these are relatively small in value and non-taxable.

Leave a comment